Articles

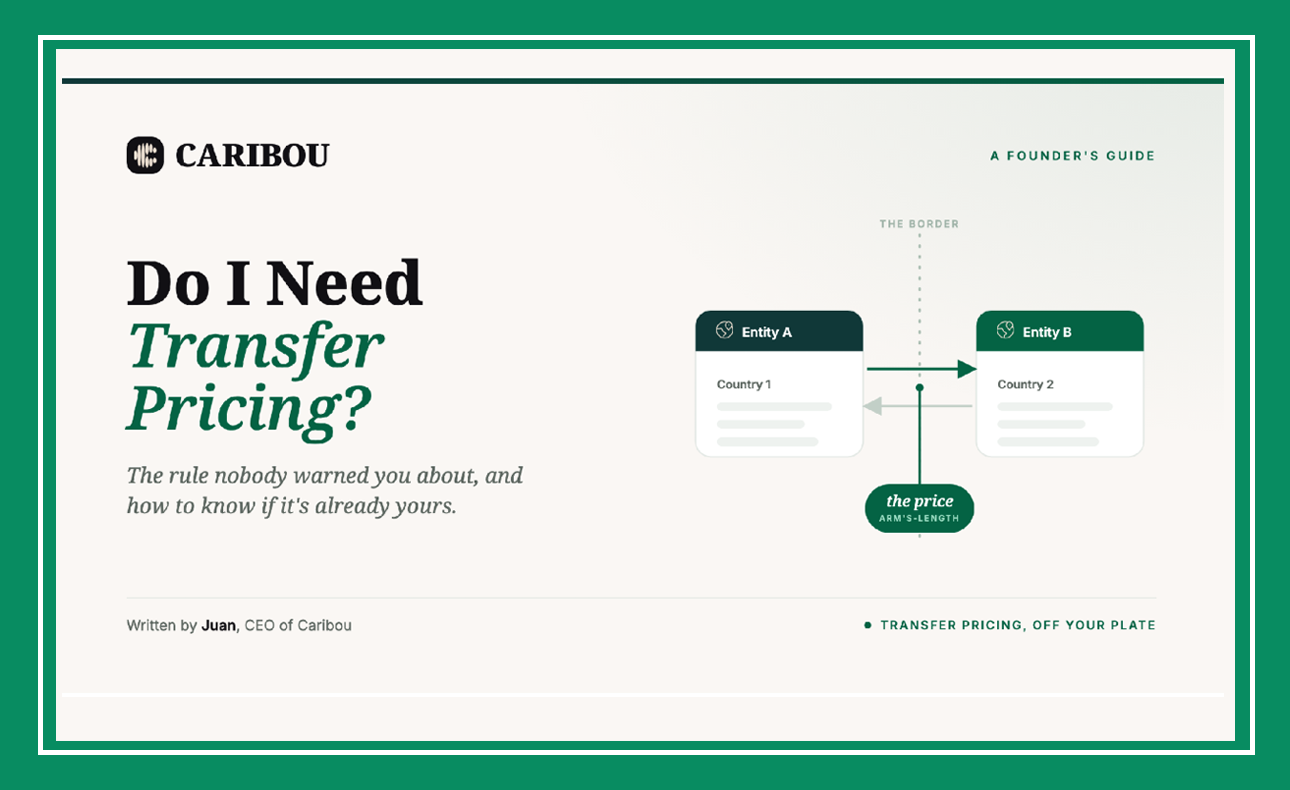

Do I Need Transfer Pricing?

A founder’s quick guide to the rule nobody warned you about Transfer pricing sounds like […]

Ash Wednesday – How the Catholic Church is Structured and Funded

Today is Ash Wednesday for Catholics. It marks the beginning of the 40-day Lenten season. […]

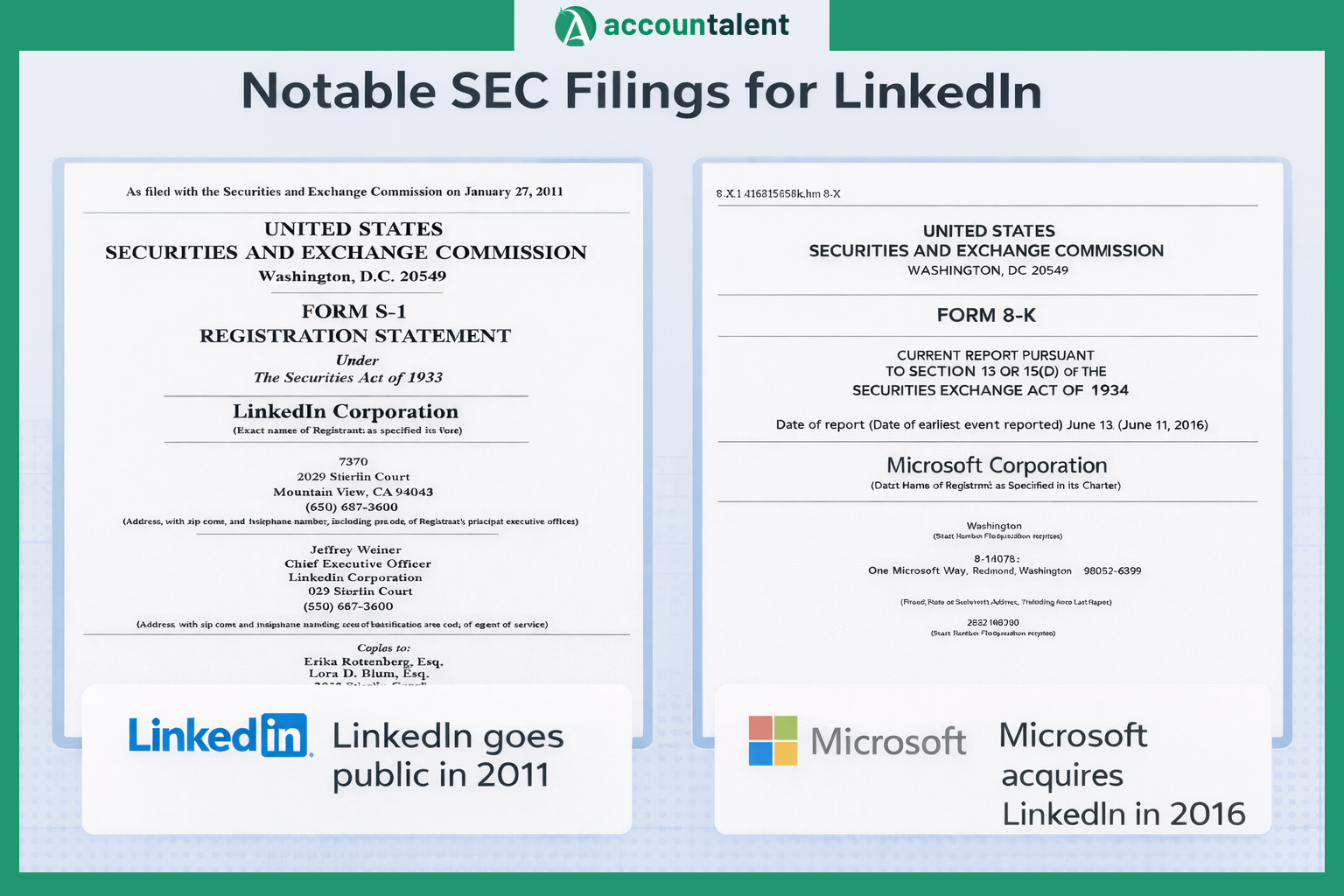

The LinkedIn Equity Story – Two Home Runs for Shareholders

The founders of LinkedIn were masters at managing equity. So, well, in fact, the shareholders […]

Do NOT “always” file an 83(b) Election

BAD ADVICE: “Always file an 83(b) Election”. For 40+ years, we have heard this guidance […]

Tax Compliance: One of the First Things Buyers Scrutinize in a Business Sale

When preparing a business for sale, one of the very first areas buyers examine is […]

Mark Your Calendars, Startups: 2026 U.S. Tax Dates You Don’t Want to Miss

Running a C-Corporation comes with its fair share of perks, but tax season doesn’t rank […]

Startup Founders – Do NOT pay yourself as a 1099 Contractor

Startup founders should not pay themselves as 1099 contractors; instead, they should be W-2 employees […]

Two Big Beautiful Tax Breaks for Startups

The Latest Startups Need to Know Re: OBBB The newly enacted One Big Beautiful Bill […]

Mark Your Calendars, Startups: 2025 U.S. Tax Dates You Don’t Want to Miss

Running a C-Corporation comes with its fair share of perks, but tax season doesn’t rank […]

When Should Startups Start Thinking About Sales Tax Compliance?

Starting a new business is an exciting journey, but it comes with a multitude of […]